For LGBTQ couples, it is important to recognize the need for custom financial planning. This becomes more important for those in a relationship that lacks the financial and legal rights of married couples.

All couples should begin their financial decision-making by discussing their individual and joint goals. As an LGBTQ couple, here are additional important considerations.

Understand Current Rights

After same-sex marriage became legal in 2015 and paved the way for all states to recognize marriage, the LGBTQ community was allowed to enjoy the social and financial benefits of marriage. For those who choose not to marry, those rights need to be addressed in alternative strategies. It is essential to know what rights are currently in place according to marital status or lack thereof, especially states that may no longer recognize domestic partnerships and civil unions now that marriage is legal. Currently, only Washington, D.C., California, Hawaii, Maine, Nevada, New Jersey, Oregon, Washington, and Wisconsin recognize domestic partnerships. Since marriage became legal, many employers no longer recognize domestic partnerships that previously provided benefits to both partners. Once the relationship status is verified, a good next step is estate planning.

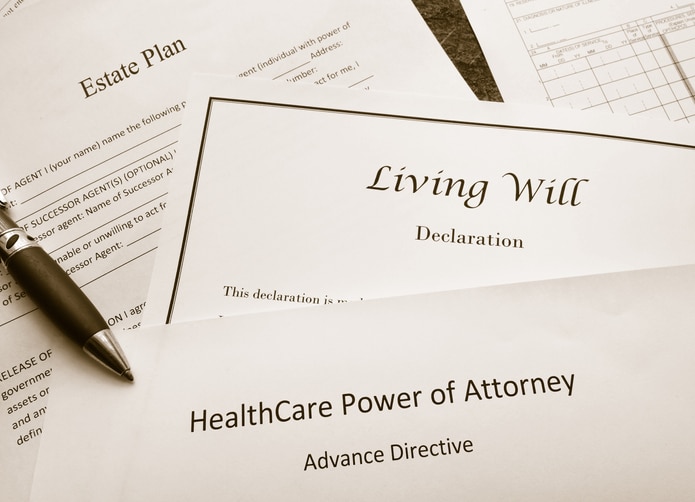

Create Estate Planning Strategies

A common misconception is estate planning is only for managing affairs at one’s death. But it is just as important while living to cover the needs of family and friends at all stages of life and grant rights to partners. These strategies can be accomplished through wills, powers of attorney, health care directives, life insurance, beneficiary designations and more. All these documents should be reviewed to align with identified values and family needs. In addition, they can prevent conflict if a family member objects to a relationship or does not have the best interest of the surviving partner in mind. For example, a parent who does not approve of a relationship may take legal action to prevent the partner from inheriting assets.

Plan for a Family

For a couple wishing to add children to their partnership, it is important to create a financial planning goal that addresses the cost. According to The Hill, a married, middle-income couple with two children would spend $310,605 to raise each newborn to age 17. [1] For gay and lesbian couples, the expense is greater when adding adoption or fertility costs. Adoption tax benefits could help to ease the financial burden. Medical procedures such as fertility methods may not always be covered by health insurance and may need to be factored into the budget.

Follow an Investment Plan

Partners should discuss and agree upon financial values to create a consistent investment strategy. If one partner is a saver and the other a spender, a financial plan can help identify changes in spending patterns that are needed to build a more stable future, especially if retirement is nearing. In addition, couples should decide whether working with an advisor who allows customized investments, such as socially responsible companies, is an important consideration. SageVest strongly recommends working with an advisor who also provides broader financial planning services.

Improve Tax Efficiency

The difference between filing taxes single versus married should be analyzed to determine a strategy to reduce taxes. While taxes should not be a driver in a relationship, partners can devise techniques that benefit them filing either way. For example, a partner who earns more could benefit from paying expenses that could be itemized and increase tax deductions. Lower income from one partner may create a tax benefit by virtue of benefiting from lower income tax brackets, by claiming deductions, or by qualifying for credits that could be lost in the event of marriage.

Protect Property Through Titling

In a marriage, spouses generally have property rights through joint ownership. As singles, only the individual owner has rights. This could cause the other partner to lose use of the property or access to funds. For example, a home owned by one partner could be sold at that partner’s death, forcing the surviving partner to leave unless proper planning mechanisms are put in place.

Reduce Risk with Insurance

One of the benefits of a financial plan is the evaluation of how a health event could harm your finances. Proper preparation with the use of insurance can be a lifesaver. Consideration should be given toward structuring health insurance coverage, disability insurance and life insurance. Even renter’s insurance plays a role for those who are not married and don’t own a home together. For example, if a fire destroyed the home, only the partner who owned the home would be covered. The non-owner partner would need renter’s insurance to cover his or her property in the home.

Overall, financial planning for LGBTQ partners and families is about ensuring each individual is provided for and protected. These are just a few points to consider for developing a financial strategy and preventing unforeseen financial obstacles. Working with an Accredited Domestic Partnership AdvisorSM (ADPA®) can help address these and many more issues specific to LGBTQ couples.

Individuals who hold the ADPA® designation have completed a course of study encompassing federal taxation, retirement planning, wealth transfers, and planning for financial and medical end-of-life needs for domestic partners. SageVest is able to serve the LGBTQ community with the help of Senior Financial Advisor Dan Serra, who is one of the few fee-only advisors to hold this designation. We invite you to contact us for more information.

Reference:

[1] https://thehill.com/policy/finance/3608647-new-estimate-projects-cost-of-raising-a-child-at-310k/