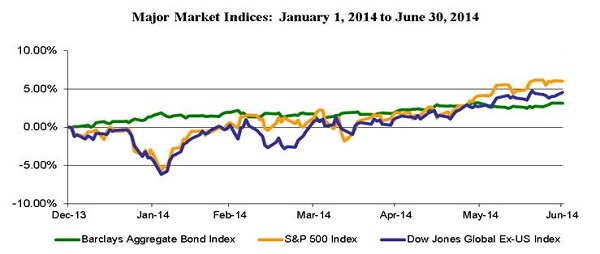

Investment markets painted a sea of green through the first half of the year as all major asset classes (stocks, bonds, commodities and real estate) were in positive territory. Stocks posted several new highs, despite advancing at a slower pace than 2013. The ‘surprise’ investment was bonds, which rallied as the 10-year Treasury rate dropped from 3% at year-end to 2.5% as of June 30th, rewarding bond owners at a time when many expected rising interest rates. Investors who remained in the markets have enjoyed positive absolute returns and an unusual level of market tranquility, offering a pleasant start to summer.

The Goldilocks Era?

With all asset classes enjoying positive performance, there has been talk of entering a ‘Goldilocks’ era – one in which everything is ‘just right’. Economic and market attributes are certainly attractive. The economy shows signs of growth, but not so much to spark inflationary concerns; volatility, measured by the CBOE Volatility Index, is at its lowest level since 2007; and central banks remain accommodative, stimulating world economies and hopefully the investment markets as well.

The US economy took pause in the 1st quarter, as reflected in the finalized -2.9% GDP figure. Our sense is that this was an anomaly as companies drew down on inventories and global exports dropped more significantly, relative to total global demand. Fortunately, current indicators are more optimistic, with job creation being the most compelling in our eyes. The unemployment rate recently declined to 6.1%, its lowest for almost six years, bringing us back in line with the long-term average over 60 years.

Looking at today’s markets, growth factors in jobs, manufacturing, housing and other key areas suggest that we may be entering an investment period similar to the mid-90’s, which was generous to investors. We are attracted to these attributes as we evaluate investment strategies, but are cautious in our optimism, largely due to asset valuation concerns.

Valuations

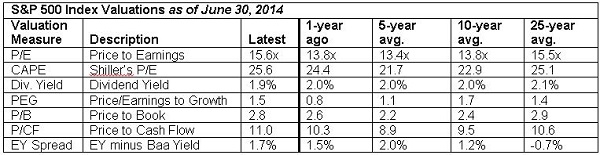

Diligent investors must evaluate if investments are reasonably priced and if they are being fairly compensated for their investment risk. In our eyes, our domestic equity markets aren’t necessarily overpriced, but they certainly aren’t cheap. The chart below shows S&P 500 index valuations using a number of measurement standards over varying timeframes. Today’s values are a bit high, relative to shorter-term averages (10 years or less), but generally fall in line with longer-term 25-year averages.

Source: Standard & Poor’s, FactSet, Robert Shiller Data, FRB, J.P. Morgan Asset Management. Price to Earnings is price divided by consensus analyst estimates of earnings per share for the next 12 months. Shiller’s P/E uses trailing 10-years of inflation adjusted earnings as reported by companies. Dividend Yield is calculated as the trailing 12-month average dividend divided by price. Price/Earnings to Growth Ratio is calculated as NTM P/E divided by NTM earnings growth. Price to Book Ratio is the price divided by next 12 months divided by price) minus the Moody’s Baa seasoned corporate bond yield. *P/CF us a 20-year avg. due to cash flow availability. Sourced from J.P. Morgan Asset Management, June 30, 2014.

It’s easier to make investment decisions when the markets appear to be undervalued or overvalued, as opposed to ‘fairly’ valued. Fairly valued stock prices generally mean we need one of two things for prices to continue rising: growth in earnings and/or a growing appetite for investment risk.

Earnings Growth:

An outlook for earnings growth based upon investment fundamentals is the most encouraging reason to invest. We’ve seen continued growth in earnings throughout the recovery, but this has largely been attributable to cost-cutting measures rather than preferred top-line revenue growth (higher sales). We believe there’s still potential for earnings growth, particularly if job creation sparks new buying demand. However, we also recognize that an improving labor market could cause wage pressures that could create a short-term hurdle for earnings until higher wages filter into the economy.

Risk Appetite:

The alternative reason that stock prices could continue rising is an increased willingness to assume investment risk. This is less preferred as it’s based upon momentum rather than improving fundamentals, but is rather plausible in today’s low interest rate environment. Ultra-low interest rates are prompting conservative investors to assume greater investment risk because they can’t afford to stay in cash or CDs where yields aren’t keeping up with inflation. Low rates are also prompting companies to issue debt and use the cash to buy back stock, creating short-term inflated stock demand.

Bond markets also suggest growing risk tolerance. The spread between rates of high yield (junk) bonds and US Treasuries is well below historical averages, meaning investors are accepting less compensation in return for greater risk. We see the same phenomenon in the international debt markets, where yields on Italian and Spanish bonds are falling near those of US Treasuries, void of currency impacts.

Looking Forward

For the remainder of 2014, SageVest Wealth Management is encouraged by signs of growth both here and abroad. However, we, and a number of investment managers represented in our investment portfolios, are growing concerned about valuations in a long bull-market cycle. Thus far, risk levels are perceived as cautionary rather than ominous, but we do feel that this environment warrants a diversified portfolio that blends growth oriented investments along with more conservative assets. This allows investors to participate in growth if we are entering a Goldilocks era, while also having elements of asset protection should risk levels begin to rise. As always, we encourage you to CONTACT US if you have any questions regarding your investments or other financial considerations.

If you found this commentary interesting, please SUBSCRIBE.